Our Marketing Team at PopaDex

How to Find Net Worth A Practical Guide to Your Finances

To figure out your net worth, you simply subtract everything you owe (your liabilities) from everything you own (your assets). This straightforward calculation, Assets - Liabilities = Net Worth, gives you the clearest possible snapshot of where you stand financially at any single moment.

Why Your Net Worth Is the True Measure of Financial Health

It’s tempting to focus on your income or how your investments are performing, but neither one paints the full picture. A high salary looks great on paper, but if it’s completely swamped by debt, your financial foundation is actually quite shaky.

Net worth cuts through all that noise. It’s not some score to beat or a way to compare yourself to others—think of it as your personal financial compass.

Once you know this number, you can start to move beyond the simple cycle of earning and spending. It shifts your focus to building real, long-term wealth. For instance, a freelancer with a choppy income can look at their net worth trend to see if their saving and investing habits are actually paying off over time, even during the lean months.

When a couple buys their first home, they see their liabilities shoot up with a new mortgage. But they also gain a massive asset. Tracking how that balance shifts over the years is incredibly empowering.

Before you start tallying up your numbers, let’s get the core components straight.

The Core Components of Net Worth

Here’s a quick breakdown of the fundamental pieces you’ll be working with.

| Component | What It Is | Simple Examples |

|---|---|---|

| Assets | Anything you own that has monetary value. | Cash in the bank, your investment portfolio, the market value of your home, your car, valuable collectibles. |

| Liabilities | Any debt or financial obligation you owe to others. | Mortgage, student loans, car loans, credit card balances, personal loans. |

| Net Worth | The final figure after subtracting your total liabilities from your total assets. | This is your personal bottom line—a direct measure of your financial position. |

With these building blocks in mind, you can start putting together a complete and honest view of your finances.

The Power of a Clear Financial Picture

Knowing your net worth gives you the clarity you need to make smart decisions. It’s the baseline that helps you set meaningful financial goals and actually measure your progress in a tangible way.

This clarity is more critical now than ever. While global wealth has exploded since 2000, a huge chunk of that growth was fueled by debt. In fact, for every $1 of wealth created through investment, about $2 in debt was also generated. You can dig into this trend and its impact by exploring the research on global wealth and debt on McKinsey.com.

This highlights a crucial point: you can’t get an accurate financial picture by only looking at your assets.

Net worth is the honest conversation you have with yourself about your money. It strips away the complexity and shows you exactly where you stand, providing the ultimate starting line for your financial journey.

When you track this number regularly, you can finally answer those big questions:

- Am I making real progress? See if your day-to-day financial choices are actually moving you forward.

- Is my debt under control? Understand the real impact your liabilities have on your overall financial health.

- Can I afford a major life change? Make confident choices about career moves, big purchases, or retirement.

By embracing this simple formula, you take back control of your financial story.

Building Your Complete Asset Inventory

Alright, we’ve covered the “why” of net worth. Now for the “what.” This is where you roll up your sleeves and get down to the business of cataloging everything you own that has real monetary value. Think of it as a personal financial scavenger hunt—the goal is to find and list every last asset.

To keep this from getting chaotic, it helps to break everything down into categories. This approach not only makes the process manageable but also gives you a much clearer picture of where your wealth is sitting. I always recommend starting with the easiest stuff first: your liquid assets.

Once you have those numbers down, you’ll move on to investments and then to your physical property, which can take a bit more legwork to value correctly. Getting this inventory right is the foundation for your entire net worth calculation.

Cash and Cash Equivalents

This is the low-hanging fruit and the perfect place to start. These are your most liquid assets, meaning you can get your hands on them quickly without a fuss. This is your financial front line.

Just log into your online banking apps and pull the current balance for each of these:

- Checking Accounts: The total cash you have across all your personal checking accounts.

- Savings Accounts: Don’t forget high-yield savings, your emergency fund, or any other savings buckets.

- Money Market Accounts: If you have one, add its current value to the list.

- Certificates of Deposit (CDs): Be sure to use their present value, not what you initially deposited.

Add those up, and you’ve just knocked out the first big piece of your asset inventory. It’s a quick win that builds momentum for what’s next.

Your Investment Portfolio

Next up: your investments. These assets are constantly changing with the market, so it’s critical to use their current market value, not what you originally paid for them. Your brokerage and retirement account dashboards are your best friends for this part.

Key Takeaway: An asset’s value is what it’s worth today, not what you paid for it yesterday. This is a crucial distinction for an accurate net worth calculation, as it reflects your current financial reality, not ancient history.

Go ahead and look up the latest values for:

- Retirement Accounts: This means your 401(k), 403(b), IRA (both Traditional and Roth), and any other company-sponsored plans.

- Taxable Brokerage Accounts: Tally up the total market value of your stocks, bonds, ETFs, and mutual funds here.

- Health Savings Accounts (HSA): If you’re smart enough to be using your HSA as an investment tool, include its current balance.

- Other Investments: This is your catch-all for things like cryptocurrency, private equity stakes, or anything else you’ve put money into.

Real Estate and Tangible Property

The final category covers your physical stuff. Valuing these items can feel a bit more subjective, but the goal here is to be realistic and rely on data wherever you can.

Let’s tackle your biggest tangible assets first:

- Primary Residence and Real Estate: For a quick but solid estimate, use online tools like Zillow or Redfin. This is usually more than enough for a personal net worth calculation; no need to call an appraiser.

- Vehicles: Jump on Kelley Blue Book or Edmunds to find the current private-party sale value for your car, truck, or motorcycle. Be honest about its condition!

- Valuable Personal Property: This includes items with real resale value, like jewelry, art, or collectibles. For really high-value pieces, you might need a recent appraisal, but for most things, a conservative estimate based on what similar items are selling for online will do the trick.

Once you have all these figures, you need a good way to organize them. To make this part easier, you can grab a dedicated net worth tracking spreadsheet that gives you a ready-made template for listing and summing everything up. This complete inventory is the crucial first half of finding your true net worth.

Getting an Honest Look at Your Liabilities

After tallying up everything you own, it’s time to face the other side of the equation. This part isn’t about judgment; it’s about getting a crystal-clear snapshot of your debts. Think of it like this: you can’t chart a course to a higher net worth until you know exactly where you’re starting from.

Precision is everything here. We’re not interested in the original loan amount or what you pay each month. What you need is the current payoff balance—the exact dollar amount required to make that debt disappear today. You can usually find this by logging into your online accounts or checking your latest statement.

Unpacking Your Secured Debts

Secured debts are pretty straightforward: they are tied directly to an asset. If you stop paying, the lender can take that asset, whether it’s your house or your car. These are often the biggest liabilities on the books, so getting the numbers right is essential.

Start by grabbing the current payoff balance for:

- Mortgage: This includes your main home loan and any home equity lines of credit (HELOCs) you might have.

- Auto Loans: List the remaining balance for every car, truck, or motorcycle loan.

- Other Secured Loans: Got a loan for a boat, RV, or another big-ticket item? Add it to the list.

Gathering these figures gives you the foundation for the liability side of your personal balance sheet.

Tallying Your Unsecured Debts

Unsecured debts are different because they aren’t backed by any collateral. Instead, a lender is trusting your promise to repay, which is why they almost always come with higher interest rates.

This category covers some of the most common types of debt:

- Credit Card Balances: Get the exact number for the total outstanding balance on all of your cards. Don’t guess.

- Student Loans: Both federal and private student loans belong here. Find the total payoff amount for each one.

- Personal Loans: Add any loans you have from banks, credit unions, or online lenders.

- Medical Debt: Don’t forget any outstanding bills from doctors, dentists, or hospitals.

Pro Tip: Worried you might have forgotten an old account? Pull a free credit report from one of the major bureaus. It lists all your open lines of credit, ensuring nothing slips through the cracks and your net worth calculation is complete.

Once you have every number, add them all up. That final figure is your total liabilities. To gain deeper insights into financial liabilities and strategies for managing them, exploring expert resources can be incredibly helpful. Honestly facing these numbers is the first, most powerful step toward making them smaller.

Sidestepping the Most Common Valuation Blunders

Calculating your net worth isn’t about being an accounting whiz. It’s really about sidestepping a few common—but costly—mistakes. Once you’ve listed out everything you own and everything you owe, the final number is only as good as the values you assign to each item. Even small errors can paint a warped picture of your financial reality, leading to bad planning and missed chances.

The most common trap people fall into is a simple one: valuing things based on what they paid for them, not what they’re worth today. Your house, your car, your investment portfolio—these are all moving targets. Their values shift constantly, so getting an accurate snapshot means using their current market value, not a number from a dusty old receipt.

Don’t Let Feelings Cloud Your Judgment

It’s incredibly easy to let emotion creep into your calculations, especially with personal items. You might think your meticulously maintained 2015 Honda is worth more than the average, or that your prized collection of vintage sci-fi novels is priceless.

For your net worth statement, though, sentimental value is always zero. The only number that matters is what a real person would actually pay you for it right now.

This isn’t about being cynical; it’s about being realistic. A net worth figure grounded in reality is a powerful tool. To keep your numbers honest:

- Be objective. Use third-party tools like Kelley Blue Book for your car or check “sold” listings on eBay for collectibles.

- When in doubt, round down. It’s always smarter to slightly underestimate an asset’s value. This builds a conservative buffer into your finances and stops you from making decisions based on inflated numbers.

Keeping an objective view is especially important when you consider the bigger picture. Globally, just 1.6% of adults hold almost 48% of all wealth. In a world with such a concentration of assets, every step you take to accurately track your own financial progress is a meaningful one. You can dive deeper into the global wealth landscape over at Voronoiapp.com.

Tackling Tricky and Illiquid Assets

Some assets just aren’t easy to put a price tag on. They often require more than a quick Google search and are a frequent source of errors when you’re figuring out how to find your net worth.

The goal isn’t perfection. It’s a reasonable, defensible estimate. Consistency in your method is far more important than chasing an exact, elusive number.

Let’s look at a few of these tricky situations:

- Your Small Business: Valuing a private business is an art and a science. For a quick estimate, you can use a multiple of its annual profit or revenue. A multiple of 2-4x annual profit is a common, conservative starting point for many small service-based businesses.

- Unvested Stock Options: This is a big one for tech employees. If you can’t sell them yet, they’re not yours. For net worth purposes, unvested options have a value of $0. Only count stocks or grants that have fully vested.

- Multi-Currency Accounts: If you have assets spread across the globe, you have to convert everything to your primary currency using today’s exchange rate. Don’t use the rate from when you first bought the asset. A quick check on a site like XE.com will give you the number you need for an accurate conversion.

Getting these details right is what separates a vague guess from a reliable financial metric you can actually use to make smart decisions.

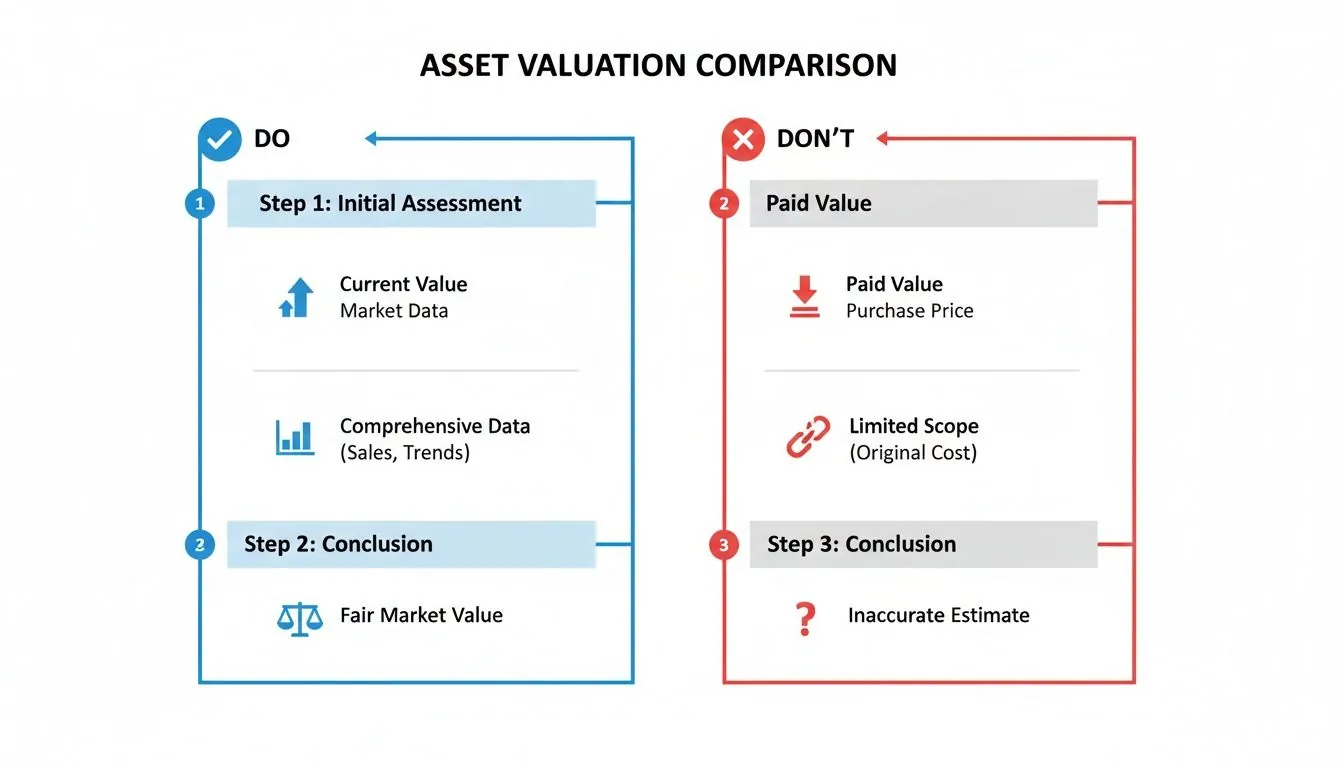

To make this even clearer, here’s a quick cheat sheet for valuing your assets without falling into common traps.

Asset Valuation Do’s and Don’ts

| Asset Type | Do This (For an Accurate Value) | Don’t Do This (Common Mistake) |

|---|---|---|

| Real Estate | Use recent comparable sales in your area or a tool like Zillow for an estimate. | Using your original purchase price from years ago. |

| Vehicles | Check Kelley Blue Book (KBB) or Edmunds for the private party sale value. | Guessing based on “how it feels” or what you wish it was worth. |

| Public Stocks | Use the current market price from your brokerage account at the close of business. | Using your cost basis (what you paid for the shares). |

| Collectibles | Look up recent “sold” prices for similar items on eBay or heritage auction sites. | Valuing them at their insured value, which is often inflated. |

| Private Business | Apply a conservative industry-standard multiple (e.g., 2-4x profit). | Valuing it based on “potential” or your emotional investment. |

| Foreign Currency | Convert all holdings to your home currency using today’s live exchange rate. | Using an old exchange rate from the time of acquisition. |

Following these simple rules helps keep your net worth calculation grounded, accurate, and truly useful for planning your financial future.

Calculating and Interpreting Your Net Worth

Alright, you’ve done the heavy lifting by pulling together your lists of assets and liabilities. Now for the easy part: the actual math. It’s time to put it all together and see what the numbers really say about your financial life.

The formula itself couldn’t be simpler: Total Assets - Total Liabilities = Your Net Worth.

Let’s walk through a quick, real-world example. Meet Alex, a marketing professional trying to get a handle on their finances.

| Assets | Value | Liabilities | Value |

|---|---|---|---|

| Checking & Savings | $15,000 | Mortgage Balance | $250,000 |

| 401(k) Retirement | $85,000 | Car Loan | $12,000 |

| Brokerage Account | $20,000 | Credit Card Debt | $4,000 |

| Home (Market Value) | $400,000 | Student Loans | $30,000 |

| Car (KBB Value) | $18,000 | ||

| Total Assets | $538,000 | Total Liabilities | $296,000 |

For Alex, the calculation looks like this: $538,000 (Assets) - $296,000 (Liabilities) = $242,000 (Net Worth).

Want to run your own numbers without breaking out a spreadsheet? A good free net worth calculator can give you an instant result.

Putting Your Final Number into Context

Getting that final number is a huge step, but on its own, it’s just a figure. The real power comes from understanding what it means for you. A big part of interpreting your net worth is simply understanding your balance sheet—that’s exactly what you’ve just created.

One of the most common mistakes people make is valuing assets based on what they paid, not what they’re worth today. This is a critical distinction.

The image drives home an essential point: current market value is what matters, not the original sticker price.

Context is everything. A negative net worth means something entirely different for a recent medical school grad buried in student loans than it does for someone a few years from retirement. For the grad, it’s a fairly normal starting line. For the pre-retiree, it’s a flashing red light signaling that some serious adjustments are needed—and fast.

Your first net worth calculation isn’t a final grade; it’s a GPS coordinate. It shows you exactly where you are so you can start mapping out the most effective route to where you want to go.

Ultimately, the number you see today is less important than the direction it’s heading. Seeing steady, upward progress over the months and years is the real goal. This simple calculation transforms from a static number into the dynamic foundation of your entire financial plan.

Automating Your Net Worth for Real-Time Clarity

Figuring out your net worth once is a great first step. It gives you a powerful snapshot of your financial health at a single moment in time.

But the real magic happens when you track it consistently. A one-off calculation is like checking the score of a game only once—you know where things stand right now, but you miss the entire story of the wins, losses, and momentum that got you there.

Let’s be honest, manually updating a spreadsheet every month or quarter gets old fast. It means logging into dozens of different accounts, digging up current values, and punching in every single number. Not only is it a time-sink, but it’s also ripe for simple typos that can throw off your entire financial picture.

The Shift to Smarter Tracking

This is exactly where modern financial tools change the game. Instead of spending hours wrangling data, you can use a platform that automatically syncs with all your financial accounts. Picture a single, clean dashboard that pulls real-time numbers from your bank accounts, investment portfolios, mortgage balance, and credit cards.

This kind of consolidated view brings some serious advantages:

- Time Savings: No more manual drudgery. You get to spend your time on strategy, not data entry.

- Improved Accuracy: Automation eliminates the risk of human error, so your numbers are always current and correct.

- Real-Time Insights: You can see instantly how market swings or a big purchase affects your bottom line.

Staying Ahead in a Changing Economy

Gaining this real-time clarity is more important than ever. Recent analysis shows that global net wealth growth has slowed to 4.4% annually, making it tougher to build wealth from market gains alone. Strategic planning and consistent tracking are your best tools for outpacing this trend. You can dive into a full breakdown of these global wealth trends on BCG.com.

By automating the process, you transform your net worth from a historical document into a dynamic, forward-looking tool. It becomes your personal financial GPS, helping you make confident, informed decisions on the fly.

Solutions like PopaDex use financial data aggregation to connect thousands of banks, manage multi-currency accounts, and give you that complete, effortless overview. This shift from manual entry to automated monitoring is the key to turning net worth tracking into a sustainable, empowering habit.

Got Questions About Your Net Worth? We’ve Got Answers.

As you start piecing together your financial picture, a few questions almost always come up. Let’s tackle them head-on so you can move forward with confidence.

How Often Should I Calculate My Net Worth?

This is a common one. While you could drive yourself crazy checking it daily, most people find that a quarterly check-in hits the sweet spot. It’s frequent enough to see how you’re tracking against your goals without getting bogged down by the market’s daily mood swings.

That said, if you’re in a specific financial season—like paying down debt with gazelle intensity or saving for a big down payment—a monthly review can be incredibly motivating. Seeing that number tick up (or your debt tick down) is a great way to stay on course.

Is It Bad to Have a Negative Net Worth?

Absolutely not, especially when you’re just starting out. Think about it: student loans, a new mortgage, a car loan… it’s incredibly common for liabilities to outweigh assets early in your career.

What matters isn’t the starting number; it’s the direction it’s moving. A net worth that is consistently trending upward over time is the real win.

Your starting point is just that—a start. It’s the beginning of your financial story, not the final chapter. Focus on progress, not perfection.

Should I Include My Home in My Net Worth Calculation?

Yes, you definitely should. Your home is likely your biggest asset, and leaving it out gives you a seriously skewed view of your financial health.

The right way to do it is to list the current market value of your home on the asset side and the remaining mortgage balance on the liability side. Sure, it’s not a liquid asset you can tap into tomorrow, but it’s a massive piece of your overall financial puzzle.

Ready to stop wrestling with spreadsheets and get a clear, real-time view of your finances? PopaDex automates the entire net worth tracking process, giving you the clarity you need to make smarter decisions. Get started for free and see your complete financial picture today.