Our Marketing Team at PopaDex

Master Budgeting with Variable Income for Financial Stability

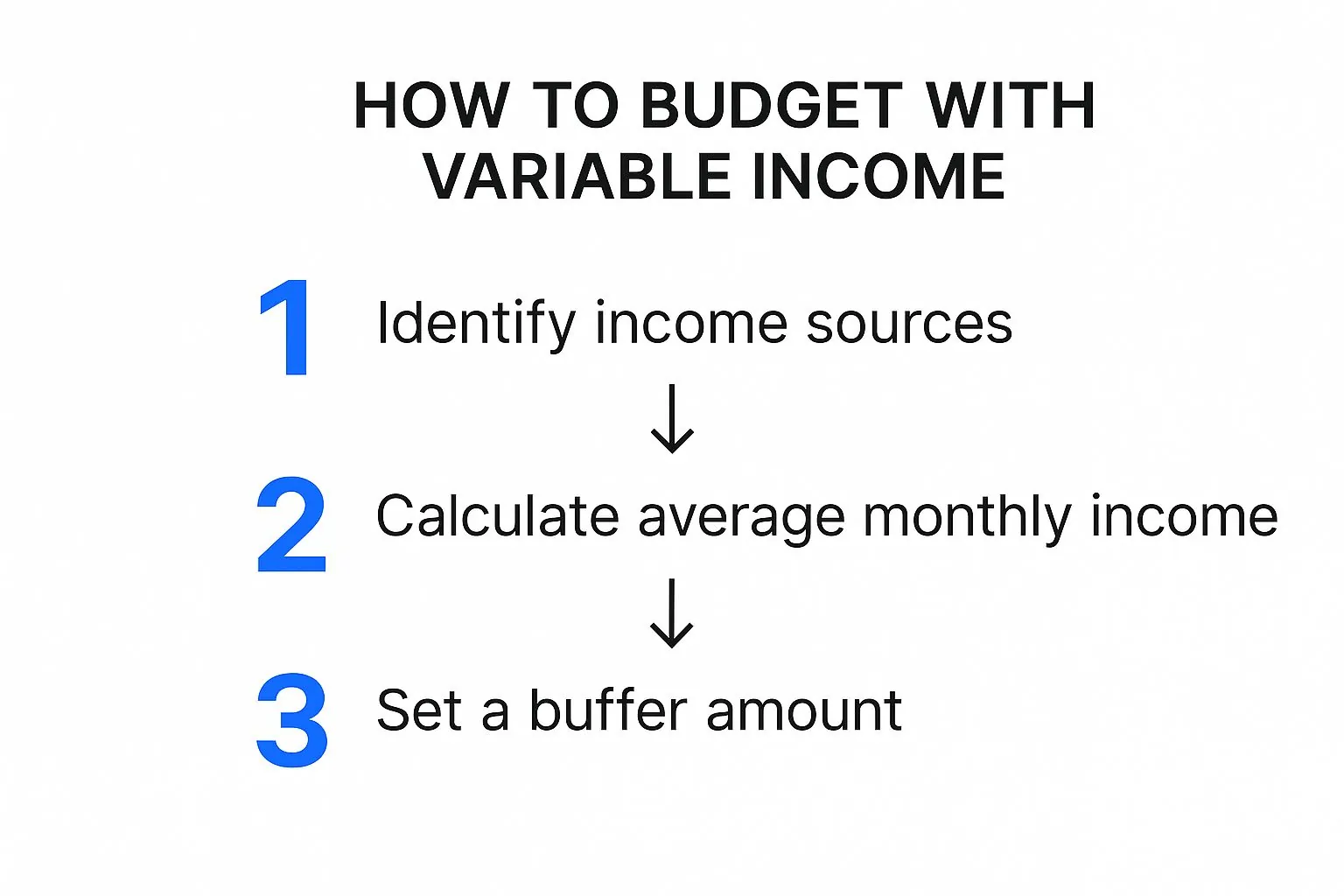

If you’re a freelancer, gig worker, or rely on commissions, you know the feeling all too well. One month you’re riding high, and the next, you’re wondering how you’ll cover rent. Budgeting with a variable income isn’t about finding a magic spreadsheet; it’s about creating a system that tames the financial rollercoaster.

The goal is to build a financial buffer that smooths out your cash flow. Instead of living in a constant state of feast or famine, you can create a predictable, stable financial life. It all starts with paying yourself a consistent “salary,” even when your earnings are anything but.

Creating Predictability From Financial Chaos

Let’s be honest: the biggest headache for anyone with a fluctuating income is the sheer uncertainty. When you have no idea what next month’s paycheck will bring, traditional, rigid budgets feel completely pointless. The real solution isn’t a more complicated budget—it’s changing how money flows into your personal life in the first place.

The most powerful strategy I’ve seen work time and time again is to create a clean separation between your business and personal finances. This means opening two distinct bank accounts. One is for all your incoming client payments and business expenses. The other is strictly for your personal life—rent, groceries, and everything else. This simple barrier is critical because it stops you from spending a big client payment the moment it hits your account.

Pay Yourself a Consistent Salary

With your accounts separated, you can now do something that feels revolutionary: pay yourself a stable, predictable salary. Take a look at your income over the past 6 to 12 months and figure out your average monthly take-home pay. This number is the new foundation for your “salary.”

Each month, you’ll transfer this exact same amount from your business account to your personal account. This is the only income your personal budget ever “sees,” and that consistency is what you need to plan effectively.

What happens in those amazing, high-income months? The extra cash stays right there in the business account, building up your buffer. And in the lean months, you’ll draw from that same buffer to pay yourself your consistent salary. It’s a game-changer.

This one shift in money management is transformative. It moves you from a reactive mindset—constantly adjusting to every financial swing—to a proactive one where you control the cash flow into your household.

This simple table breaks down how to turn your unpredictable earnings into a steady paycheck.

From Variable Income to Stable Paycheck

This table outlines the core steps to create a predictable ‘salary’ from your fluctuating income, making your personal budget easier to manage.

| Step | Action | Why It Works |

|---|---|---|

| 1. Analyze Past Income | Calculate your average monthly take-home pay over the last 6-12 months. Be realistic. | This gives you a data-backed number for your “salary,” not a hopeful guess. |

| 2. Separate Accounts | Open a dedicated “business” account for all income and a “personal” account for living expenses. | It creates a crucial psychological and practical barrier, preventing you from spending windfalls impulsively. |

| 3. Set Your Salary | Choose a conservative, consistent amount to transfer from your business to your personal account each month. | This creates the predictability your personal budget needs to function properly. |

| 4. Build a Buffer | In high-earning months, leave the surplus cash in the business account. | This surplus becomes your safety net, covering your salary during lower-income months. |

| 5. Stick to the System | Treat your salary as your only income for personal budgeting. Never spend directly from the business account. | This discipline is what makes the entire system work and eliminates the feast-or-famine cycle. |

By following these steps, you build a robust system that insulates your personal finances from the volatility of your work. It’s about creating your own stability.

This process shows how identifying your income, calculating a realistic average, and setting up a buffer creates a reliable financial baseline. It’s a foundational practice for anyone trying to get a handle on inconsistent earnings.

The Power of a Financial Buffer

Tackling inconsistent cash flow is the main event here. Recent data from the Bureau of Labor Statistics shows that while average income growth has been outpacing spending, there are huge differences between income levels. This really drives home how households with fluctuating earnings struggle to match their spending with their income. It highlights just how critical flexible budgeting and a solid savings buffer are to get through those lean periods.

To build a strong foundation, it helps to learn from proven methods, like those in guides on how to create a family budget that works long-term. Adopting this “pay yourself first” approach offers incredible benefits, both practically and psychologically. You get peace of mind knowing your essential bills are covered, no matter how slow the month is, and you can finally build a budget that actually works.

Pinpointing Your True Cost of Living

Before you can get a handle on a fluctuating income, you have to know—down to the dollar—what it costs to just be you for a month. This isn’t about guesstimates or what you think you spend. It’s about finding your baseline survival number.

Think of this number as the financial bedrock for every decision you make, especially when you hit a lean month. It’s the absolute minimum you need to keep the lights on and your life running.

To find it, you’ll need to play financial detective for a bit. The mission is to track every single dollar that leaves your accounts. This goes beyond big categories; it’s about seeing where your money actually goes. You can use a simple notebook, a spreadsheet, or an app like PopaDex to make it happen. Honesty is non-negotiable here.

Sorting Your Fixed and Variable Costs

First things first, let’s dump all your expenses into two buckets: fixed and variable. This simple act is the cornerstone of budgeting with an unpredictable income because it shows you what’s set in stone versus where you have room to maneuver.

Fixed expenses are the bills that show up like clockwork for the same amount every month. They’re predictable and form the core of your financial responsibilities.

- Rent or Mortgage: Your biggest, most predictable housing cost.

- Loan Payments: Car loans, student debt, or personal loans.

- Insurance Premiums: Health, auto, or renter’s insurance.

- Core Subscriptions: That essential software for work or the one streaming service the family can’t live without.

These are your top priority. Add them all up, and you’ve got the first piece of your baseline puzzle.

Variable expenses are the costs that are necessary but change from month to month. These are the budget-busters if you aren’t paying attention. One month your groceries might run you $400, and the next it’s $550 because you hosted a dinner party.

Key Takeaway: Understanding the difference between fixed and variable spending is everything. Fixed costs are your foundation. Variable costs are where you find the flexibility to adapt when income dips.

Calculating Your Baseline Number

Once you’ve tracked your spending for two or three months, you can nail down your baseline number with real confidence.

For your fixed costs, just add them up. It’s a single, reliable figure. For your variable expenses—like groceries, gas, and utilities—don’t just pick your best month. That’s a recipe for disaster. Instead, calculate a three-month average to get a much more realistic picture of your typical spending.

Here’s what that looks like in practice:

| Expense Type | Example Costs | Monthly Total |

|---|---|---|

| Fixed Expenses | Rent: $1,500, Car Loan: $300, Insurance: $150 | $1,950 |

| Variable Expenses | Groceries (avg): $450, Gas (avg): $150, Utilities (avg): $200 | $800 |

| Total Baseline | $2,750 |

This $2,750 is your magic number. It’s your baseline. This is the minimum amount you need to “pay yourself” from your business account to cover your non-negotiables and essential living costs.

Suddenly, it’s not just a number on a spreadsheet. It’s a concrete target that brings clarity to the chaos, giving you the power to know exactly how much of a buffer you need to build for those inevitable slow seasons.

Choosing a Budget That Bends Without Breaking

When your income changes month to month, a rigid, unforgiving budget is your worst enemy. Trying to force fluctuating earnings into a fixed structure is a fast track to frustration and, ultimately, giving up.

The real key is to find a system that’s built for flexibility. You need something that can expand during the high-income months and hold firm during the lean ones. Your goal is more than tracking spending—it’s to build a financial framework that actually supports your unique rhythm.

Let’s walk through three popular budgeting methods and, more importantly, how to adapt them for an irregular income stream.

The Zero-Based Budget, Reimagined

At its core, zero-based budgeting is simple: you give every single dollar a job until your income minus your expenses equals zero. For anyone with a variable income, this monthly reset is an incredibly powerful tool. Instead of trying to plan a full year out, you plan for the money you have right now.

Let’s say you’re a web developer who just landed a $7,000 payment for a big project. Your baseline monthly expenses, however, are only $3,000. Here’s how you could put a zero-based approach into action:

- Cover Your Baseline: First things first, allocate $3,000 to cover all your essential fixed and variable costs for the month.

- Fund Your Buffers: Next, make an aggressive move. Send $2,000 straight to your tax savings and emergency fund.

- Invest for the Future: Put $1,000 into a retirement or investment account.

- Enjoy the Surplus: That last $1,000? It’s now assigned to guilt-free “wants”—a new gadget, a weekend trip, or some nice dinners out.

If next month you only earn $3,500, your plan will look completely different, and that’s the point. This method forces you to be intentional with every windfall and stay disciplined during the slower periods.

Adapting the 50/30/20 Rule

The classic 50/30/20 rule is a fan favorite for a reason: it’s simple. The rule suggests putting 50% of your income toward needs, 30% toward wants, and 20% toward savings. But this fixed-percentage model can fall apart fast when your income drops unexpectedly.

The fix? Apply the percentages to your stable salary—the consistent amount you pay yourself—not your total fluctuating income.

Imagine you pay yourself a steady $4,000 per month. Your adapted budget would look like this:

- 50% Needs ($2,000): This covers the non-negotiables like rent, utilities, and groceries.

- 30% Wants ($1,200): Here’s your budget for hobbies, entertainment, and dining out.

- 20% Savings ($800): This chunk goes directly to debt repayment or investments.

By basing the 50/30/20 rule on your predictable “paycheck” instead of your gross earnings, you create a sustainable plan. The surplus cash left in your business account during high-income months is then used to build your larger financial safety nets, completely separate from your personal monthly budget.

The “Pay Yourself First” Model, Perfected

This is more than a catchy savings phrase; for those with a variable income, it’s a genuine survival strategy. While we’ve already touched on paying yourself a salary, this model takes it a step further by prioritizing savings before a single dollar gets spent elsewhere. The moment your “paycheck” hits your personal account, automated transfers should be whisking money away to your high-priority goals.

This strategy becomes even more critical on a global scale. IMF data shows that income volatility is far more pronounced in emerging markets than in advanced economies like the G7 countries. For households in low-income developing nations, where per capita incomes are below roughly $2,390, managing huge income swings is a fact of life. For them, aggressive savings is more than good advice—it’s essential for stability.

This is the go-to approach for many freelancers and small business owners. For a deeper look into financial systems designed specifically for self-employment, check out our complete guide on https://popadex.com/budgeting-for-freelancers/.

Ultimately, it doesn’t matter which method you choose. The right budget is the one you can actually stick with—one that provides both structure and the grace to adapt when life happens.

Building Your Financial Safety Net

When your income is all over the map, your best defense isn’t a rigid, complicated budget—it’s a smart financial buffer. I’ve learned that building this multi-layered safety net is the single most important step for anyone with a variable income. It’s what gives you the stability to ride out those lean months without spiraling into stress or debt.

The whole process comes down to creating two different kinds of savings: one for genuine, out-of-the-blue emergencies, and another for those big, predictable expenses you know are lurking around the corner. Getting this system right is what separates people who feel in control from those who are always one bad month away from a full-blown panic.

The Foundation: Your Emergency Fund

First things first, let’s talk about your emergency fund. This isn’t your vacation fund or your new-laptop fund. This money is exclusively for unexpected, urgent crises—think a sudden job loss, a medical emergency, or a busted water heater that floods your kitchen.

The goal is to sock away 3 to 6 months’ worth of your baseline living expenses—that bare-bones number you figured out earlier. A solid emergency fund is non-negotiable for a strong financial safety net. If you’re starting from scratch, this guide on how to start an emergency fund is a fantastic resource.

I know, that number can feel intimidating. Don’t try to fund it all at once. Start with a smaller, more achievable goal, like getting your first $1,000 saved up. When you have a great income month, be aggressive and throw a larger chunk in. Even small, steady deposits during average months will build powerful momentum. The most important rule? Keep this money separate and treat it as sacred.

An emergency fund is your financial firewall. It’s the one thing that protects your long-term goals from getting wiped out by short-term chaos. It’s the buffer that lets you think clearly when everything else goes wrong.

The Power of Sinking Funds

Okay, so an emergency fund covers the unexpected. What about the inevitable? That’s where sinking funds come in. Think of these as targeted savings buckets for large, predictable expenses that don’t hit your budget every month.

I’ve seen these work wonders for freelancers and business owners. Some of the most common sinking funds include:

- Quarterly Taxes: If you’re self-employed, you know the quarterly scramble all too well. A dedicated tax fund puts an end to that.

- Annual Insurance Premiums: For those chunky car or home insurance bills that only show up once or twice a year.

- New Equipment: Maybe it’s a new work computer or a camera that’s vital for your business.

- Car Maintenance: For that set of new tires or a major service you know is on the horizon.

The strategy is beautifully simple. Calculate the total expense, then divide it by the number of months you have left to save. For example, if you anticipate owing $2,400 in taxes in six months, you’d aim to set aside $400 each month. This proactive approach turns a massive, gut-wrenching bill into a manageable, planned expense.

To make tracking these funds a whole lot easier, a good template is a game-changer. Our free irregular income budget template is designed specifically for this, helping you see exactly where you stand with each of your sinking funds.

Mastering the Feast and Famine Cycle

Let’s be real: budgeting with a variable income is more than tracking expenses. It’s about creating a concrete, actionable game plan for your best months and your worst. This is how you trade financial anxiety for genuine control, turning those high-income periods into a foundation for long-term security.

Instead of trying to make every month look the same, think of your money in two distinct modes: “Feast Mode” for when the cash is flowing, and “Famine Mode” for when things are tight. Having a specific strategy for each is what finally creates stability.

Capitalizing on Feast Months

When a great month hits, the temptation to immediately upgrade your lifestyle is powerful. But the smartest thing you can do is stick to a strategic waterfall of priorities. This approach ensures every extra dollar is put to work for your future before you spend it on today’s wants.

Think of it as a strict order of operations for any surplus cash:

- Cover Your Baseline: First things first, pay your normal monthly “salary” into your personal account. All your standard bills and living costs are covered. No exceptions.

- Aggressively Fund Buffers: Now’s your chance. Make a significant deposit into your emergency fund and any sinking funds you have (like for taxes, a new car, or a holiday).

- Attack High-Interest Debt: Use the extra cash to make a real dent in credit card balances or personal loans. Every dollar you pay down now saves you money on interest later.

- Invest for Growth: Once your buffers are healthy and toxic debt is handled, it’s time to put money toward your long-term retirement or investment goals.

- Enjoy Guilt-Free Spending: Finally, with all the important work done, you can confidently and shamelessly enjoy what’s left over.

This structured flow is how you systematically build wealth and security, making sure your good fortune actually lasts.

Your strategy during high-income months has the biggest impact on your long-term financial health. It’s where you build the defenses that will protect you during the inevitable lean times.

Navigating Famine Months

When income inevitably dips, your strategy flips from offense to defense. The goal is simple: protect your financial core and get through the month without losing ground. With a predetermined plan, panic never enters the equation.

During a low-income month, your financial moves should be focused and minimal.

- Cover Only the Essentials: Your focus narrows to just your baseline survival number—rent, essential utilities, groceries. All discretionary spending goes on hold.

- Draw from Your Income Buffer: This is precisely why you built that buffer in your business account. You use it to pay your normal “salary” to yourself. Critically, you are not touching your core emergency fund. That’s sacred, reserved for true, unexpected emergencies only.

- Postpone Non-Essentials: Any extra contributions to long-term investments or aggressive debt pay-down (beyond the minimum payments) are temporarily paused.

This defensive posture is absolutely essential. The challenge of managing a fluctuating income is felt everywhere, but it’s especially tough in different economic climates. In the EU, for instance, households dedicate over 60% of their spending to just housing, food, and transport. The 2020 Household Budget Survey from Eurostat shows that the top 20% of earners spend more than double what the bottom 20% do, which puts a spotlight on the intense pressure faced by those with variable incomes. This disparity proves why having a solid defensive plan for lean months is non-negotiable.

By having clear rules for both feast and famine, you create a system that can weather any storm. This dual strategy is the secret to finally taming your budget and achieving real, lasting financial peace. For a deeper dive, check out our guide to mastering budgeting for financial freedom.

Even with the best-laid plans, budgeting on a fluctuating income always throws a few curveballs. It’s one thing to have a system, but it’s another to know how to react when real life happens.

Let’s walk through some of the most common questions that pop up and get you some clear, practical answers.

How Should I Save for Quarterly Taxes?

Forgetting about taxes is the classic freelancer nightmare. One minute you’re celebrating a great month, the next you’re hit with a massive bill you can’t pay. The simplest way to avoid this shock is with a dedicated tax sinking fund.

Here’s how it works: Every time a client pays you, immediately slice off a percentage—a good starting point is 25-30%—and move it into a separate high-yield savings account labeled “Taxes.” This isn’t your money. It’s just passing through your hands on its way to the government. Internalizing that fact is half the battle. When those quarterly deadlines hit, the money is just sitting there, ready to go. No stress, no scramble.

What’s the Best Way to Handle a Big Unexpected Expense?

This is exactly why you built an emergency fund. If a truly unexpected, major expense hits—think a blown car engine or a sudden medical bill—that’s your go-to account. Use it, and don’t feel guilty about it.

The crucial next step is to make replenishing that fund your absolute top priority. The very next time you have a high-income month, funnel your surplus cash into rebuilding it before you put money toward any other goals. This discipline is what keeps your financial safety net strong.

Your emergency fund is for true, unforeseen crises. Your income buffer in your business account is for smoothing out normal income dips. Knowing which one to use protects your long-term financial stability.

Debt Repayment or Emergency Fund First?

It’s a hot debate, but for anyone with a variable income, the answer is crystal clear: prioritize a starter emergency fund first. Your initial goal should be to save at least $1,000 to $2,000 before you start aggressively tackling debt.

Without that small cash cushion, any unexpected expense will send you right back into debt, completely erasing your progress. It’s a frustrating cycle. Once you have that initial buffer, you can pivot to attacking high-interest debt while continuing to build your full emergency fund at a slower pace. It’s a balanced strategy that protects you from those inevitable setbacks.

Ready to stop guessing and start seeing your entire financial picture with clarity? PopaDex gives you the tools to track every account, monitor your progress, and build a budget that finally works with your variable income. Take control of your finances today at https://popadex.com.