Our Marketing Team at PopaDex

How to Build Wealth Fast With Proven Strategies

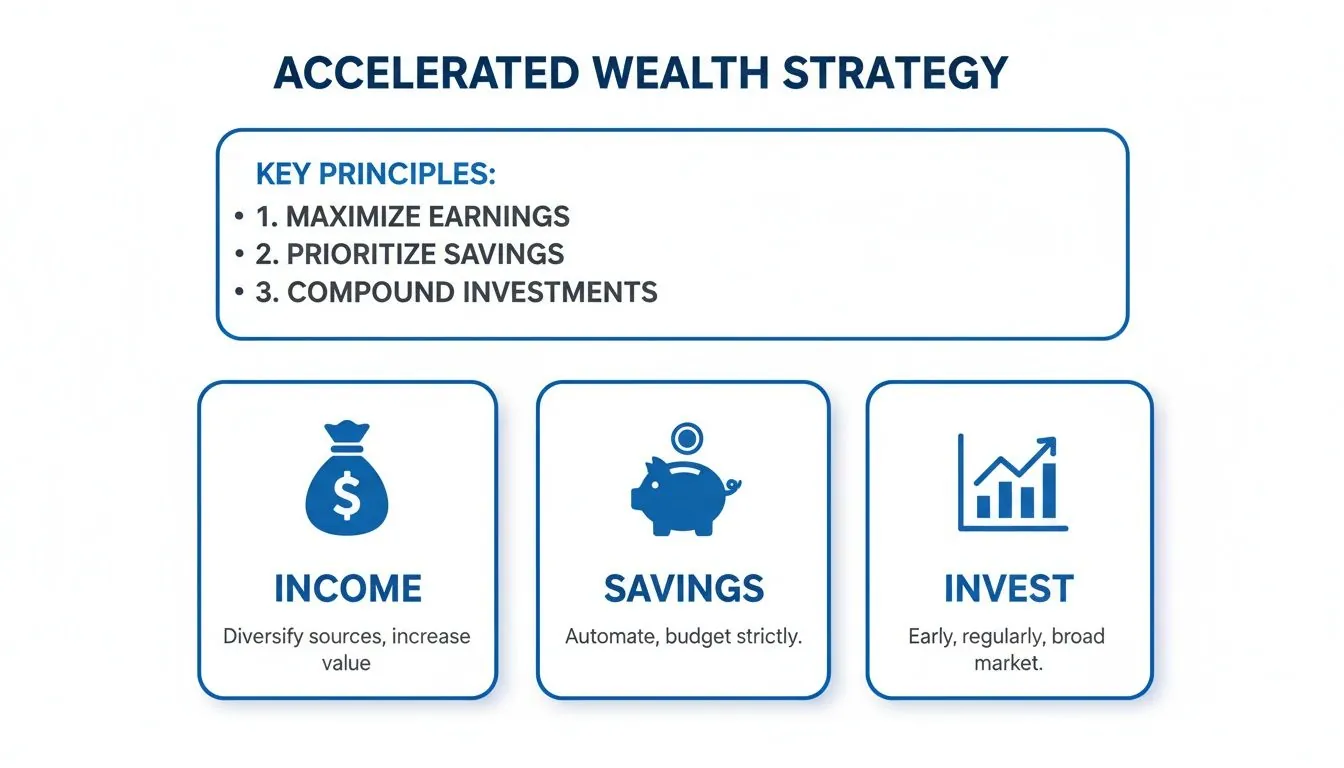

Fast Wealth Building Overview

Building wealth quickly is about boosting your earnings, trimming high-interest debt, and channeling funds into assets that grow. Many freelancers start weekend gigs and see an extra $20K+ within 18 months, then funnel those gains into rental properties or broad-market index funds. That combination accelerates net worth faster than any single tactic.

Key Pillars Of Fast Growth

- Boost Income through well-chosen side hustles and confident pay negotiations

- Maximize Savings by cutting nonessentials and automating transfers into dedicated accounts

- Allocate Capital into high-impact vehicles like equities or real estate, based on your risk comfort

By the end of 2024, global financial wealth topped $305 trillion, while private household assets reached €269 trillion, driven largely by North America. Discover more insights about global wealth growth

Below is a snapshot of the main approaches so you can weigh timing, capital needs, and risk.

Summary Of Wealth Building Strategies

Here’s a quick introduction to how each tactic compares across timelines, starting capital, and benefits.

| Strategy | Timeline | Required Capital | Risk Level | Key Benefit |

|---|---|---|---|---|

| Side Hustles & Negotiations | 6–18 months | Low | Medium | Rapid cash flow boost |

| Savings Automation & Debt Paydown | 3–12 months | Minimal | Low | Frees up investable income |

| High-Impact Investing | 1–5+ years | Varies | High | Accelerated net worth appreciation |

Each route offers distinct advantages—combine tactics based on your starting point and goals.

Applying The Infographic

This visual breaks down income, savings, and investing levers in order of impact. Use it to decide whether you need a stronger side gig or should focus on cutting costs first.

Aim for a balanced mix: push earnings, pay down debt, then let your investments compound.

Testing Scenarios With PopaDex

Run quick “what-if” savings and investment mixes on PopaDex to see projected net worth over time. For example, putting €5,000 into a side-gig that returns 20% annually can unlock new capital for real estate or stock index funds by year two. Use the Disposable Income Calculator to identify how much you can safely redirect each month.

Decide your launch plan, map out your next 6–18 months, and start building momentum today.

Boost Income Through Multiple Channels

Relying on a single paycheck rarely gets you to those fast-wealth goals. Mixing a solid salary increase with creative side projects can really speed up your journey.

Negotiating a 15% raise might only take an hour, but it adds up to thousands more each year. Meanwhile, a weekend consulting gig can turn into $10K in extra income before you know it.

- How I turned a Saturday morning design request into a five-figure freelance business using free tools and minimal overhead

- A negotiation framework that helped a colleague secure a 15% bump in under an hour

- My affiliate marketing setup that yields 5–10% commissions on honest product reviews

- Building and launching a Udemy course for recurring revenue every month

Each opportunity comes with its own setup time and risk profile. Laying out realistic timelines lets you tackle the highest-impact channels first.

Pairing two or three gigs also cushions you against income dips. Those extra dollars can be reinvested, compounding your returns in just a few months.

Real World Income Scaling Comparison

| Channel | Setup Time | Initial Cost | Annual Return |

|---|---|---|---|

| Salary Negotiation | 1–2 weeks | $0 | 15% bump |

| Weekend Freelance | 3–4 weeks | <$100 | $10K+ |

Take a designer I know: she started selling logo templates in her evenings and hit $5K in the first three months. By month six she added social media kits and doubled her revenue.

A simple script—“I’d value a compensation review once I hit these milestones”—made bold asks feel natural.

“Diversify your income and shield yourself from setbacks”

– Freelance Consultant

Once your active work hums along, layer in passive streams. Affiliate links tucked into trusted reviews often deliver 5–10% commissions with almost zero upkeep.

You might also want to check out our article on Passive Income Ideas for Beginners to fuel your passive streams.

Creating an online course takes effort up front—clear outlines, engaging videos, interactive quizzes—but no inventory means low risk. One coach I advised pulled in €8K within two months on Udemy.

Minimal hosting fees and automation tools handle enrollments 24/7, so you stay focused on content updates.

Steps To Negotiate Salary Increase

- Research market rates and pin down your target range

- Document three standout achievements, each backed by data

- Schedule a chat with your manager and lead with confidence

- Follow up in writing, proposing next steps and timelines

This framework helped a software engineer land a 15% raise in four weeks. That extra cash jump-started her first freelance website.

Tracking every penny across gigs is simple with a spreadsheet or a tool like PopaDex. Visual dashboards show net gains, compare metrics, and flag underperformers instantly.

Consistency wins when you juggle multiple streams. Set weekly goals, block out dedicated time slots, and use calendar reminders to stay on track.

“Earnings diversity smooths out financial peaks and valleys”

– Entrepreneur

Then turn surpluses into growth assets fast. Allocating just 20% of your side income into low-cost index funds can turbocharge your net worth.

Reinvesting profits also boosts your credibility for premium offerings. Clients notice a proven track record and pay more for established brands.

In under a year, someone I coached grew side income to €12K by cross-selling design and copywriting services. That extra cash then became a rental deposit.

Balanced Income Strategy

A blend of salary, freelance, and royalties smooths out your growth curve. Diversified revenue streams reduce stress and keep cash flow predictable.

Use PopaDex to track everything in one place. Visual charts reveal top performers and highlight where you can cut losses.

Monthly check-ins ensure you’re moving toward those fast-wealth targets. Tweak your tactics based on real data, not guesses.

Spreading your earnings across channels also makes tax season far less painful. Follow this roadmap and watch how building wealth fast becomes more than a theory—it turns into your everyday reality.

- Negotiate salary bumps aiming for 10–20% annually

- Launch at least one side gig with low startup costs and high skill alignment

- Reinvest 20% of side earnings into growth assets

- Track all income streams on a weekly basis

Maximize Savings And Prioritize Debt Repayment

Small tweaks to regular spending can unlock big results. By trimming nonessential costs, you boost your savings rate almost instantly. That extra cash is your ticket to paying down debt faster and putting money to work.

I’ve seen one household slash their dining-out budget from $200 to $100 each week. That alone freed up $600 a month, which went straight on to their highest-interest credit card.

Now, you don’t have to pick just one way to budget. Comparing different methods will show what clicks for you. Some people swear by zero-based budgeting, others feel relief with envelopes, and plenty of folks let automation handle the heavy lifting.

Key Budgeting Hacks

-

Zero-Based Budgeting

Assign every dollar a purpose. One couple tracked expenses to the cent and recovered 15% of their income. -

Envelope Method

Split cash into physical envelopes for each category. When it’s gone, you stop spending. -

Automated Transfers

Have a portion of your paycheck jump straight into savings. An automated sweep once helped a family stash 20% of earnings before bills.

“When you make your budget automatic and nonnegotiable, you win without thinking.”

– Seasoned Financial Coach

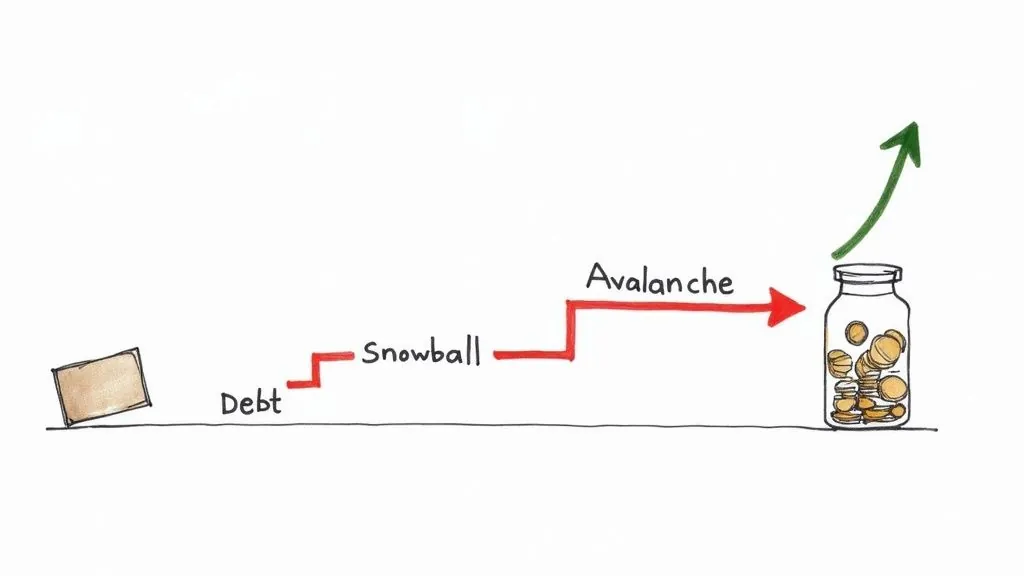

Debt Payment Strategy Comparison

Tackling debts with either small-balance wins or highest-interest targets can accelerate your net worth growth. Here’s how they stack up:

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Primary Focus | Smallest balances | Highest interest rates |

| Motivation Style | Quick, visible wins | Lower total interest |

| Estimated Interest Saved | Moderate | $1,250 on $20K |

| Payoff Time on $20,000 Debt | ~3 years | ~2.8 years |

With an $20,000 balance at 18% APR, avalanche saves you about $1,250 versus snowball. But some find the disappearing-balance thrill more motivating with the snowball.

Automating Your Debt Paydowns

Automation removes guesswork and keeps you on track. Missing payments becomes a thing of the past, and your balances shrink on their own.

- Link one checking account to all creditors.

- Schedule transfers right after payday.

- Throw extra payments at the highest-interest account while covering minimums on the rest.

- Bump up each payment by 1–2% of income every few months.

In one real-world example, this approach unlocked an extra $300 per month in free cash. Within six months, that money was funding new investment opportunities.

You might also enjoy our deep dive on mastering payment plans. For a thorough walkthrough, check out accelerating your debt payoff journey.

Allocating Savings To Investments

Once you’ve wrangled your debt, the next step is making your money work harder. Start by funneling freed-up cash into tax-smart accounts—think IRAs or low-cost brokerage accounts. I watched a client shift $500 a month from loan payments into index funds and earn a 7% average return.

- Track everything in PopaDex to keep your plan transparent.

- Use the disposable income calculator to nail down your contributions.

- Set up recurring buys to benefit from dollar-cost averaging.

“Reinvested savings are the fuel that powers rapid wealth building.”

– Veteran Wealth Advisor

Imagine being debt-free in a year. That reclaimed $500 each month could grow to more than $20,000 in a decade at 8% returns. It’s the kind of compound effect that makes tightening the belt worth every penny.

By combining disciplined budgeting, focused debt payoffs, and swift investment moves, you lay out the fastest path to building serious wealth. Keep PopaDex open, let alerts nudge you when you veer off track, and review your progress weekly. Hit your targets and watch your net worth climb.

Deploy Capital Into High-Impact Investments

You’ve built up your cash reserves and made serious progress on debt. Now it’s time to turn that dry powder into meaningful growth. By blending a dose of conviction plays with broad diversification, you capture upside without courting disaster.

Take one concentrated stake in a startup that went on to return 12x over ten years. Eye-opening, right? Yet you’ll sleep better at night knowing the rest of your portfolio cushions any single slip.

Public Equity Strategies

Public stocks remain the easiest way to tap into decades of compound returns and instant liquidity.

Consider pairing low-cost index funds that target 7–10% annual gains with deep dives into a handful of high-growth names.

Since 1926, U.S. equities have created roughly $47.4 trillion in net wealth—and the top 2.4% of firms accounted for nearly all of it over a 30-year span. Read the full research about concentrated equity wealth creation

- Large-Cap Index Funds for instant, hands-off market exposure

- Individual Equity Positions when you’ve got time for rigorous research

- Thematic ETFs to zero in on areas like biotech or clean energy

Private Equity And Venture Capital

Allocations here can dish out 20–30% IRRs, but expect capital lock-up for years. If you qualify, consider joining a club deal to pool resources into pre-IPO rounds.

• Vet fund track records and realized multiples

• Benchmark fees against peers

• Understand expected exit timelines and secondary options

Alternative Assets And Diversification

Real estate, commodities or art often move independently of stocks—and they can soften equity swings.

| Asset Class | Time Horizon | Liquidity | Risk Level | Return Potential |

|---|---|---|---|---|

| Public Equity | 5+ years | High | Medium-High | 7–10% avg |

| Private Equity | 7+ years | Low | High | 20–30% IRR |

| Real Estate | 10+ years | Medium | Medium | 8–12% IRR |

Aim for a 2–5% slice of each alternative to balance firepower with flexibility.

A well-measured allocation keeps growth on track without trapping your cash.

Tax Efficiency And Rebalancing

Every dollar you shelter from taxes adds to your compounding engine.

- 401(k) & 403(b) plans defer taxes and may include employer matches

- Traditional IRA contributions can reduce taxable income today

- Roth IRA balances grow tax-free, perfect for long-term withdrawals

Block out two dates per year to rebalance and buy into oversold areas. In taxable accounts, tax-loss harvesting shields gains and boosts after-tax returns.

Putting It All Together

PopaDex dashboards make your allocation plan visible at a glance.

- Define target weights for each asset class based on your risk comfort

- Automate purchases into low-cost funds on a recurring schedule

- Set PopaDex alerts for drift beyond 5% of targets

- Review results every quarter and tweak as needed

Following this playbook shows exactly where to deploy your capital and when to circle back for adjustments.

Real World Allocation Example

Picture a $100,000 portfolio split into 60% public, 20% private and 20% alternatives. Over ten years, you’d aim for a 12% annualized return after fees.

If one private deal doubles, it more than covers broad-market lags.

- Vet managers with third-party audits

- Favor clear, transparent fee structures

- Cap any single position at 10% of net worth to avoid outsized concentration

Real estate can add 8% net yields, but watch local cycles. And steer clear of high-leverage loans when markets are frothy.

Consider Liquidity And Risk

Holding dry powder means you can pounce on bargains when they appear.

- Keep 5–10% in cash or short-duration bonds

- Use stop-loss rules for individual equity bets

- Reserve a 10% buffer for unexpected needs

PopaDex’s drawdown tracker lets you know the moment your lineup drifts. Public stocks compound patiently, while VC and PE demand patience—so keep your timelines realistic and revisit targets annually.

Start deploying your capital today with confidence.

Leverage Real Estate And Entrepreneurial Ventures

Using borrowed capital in property and business can accelerate your wealth-building by boosting returns on modest capital.

A mortgage with a low interest rate lets you control an asset far beyond your initial down payment.

Entrepreneurs who plow early profits back into growth often see equity compound faster than what traditional savings accounts can deliver.

Rental Yield Analysis Methods

One investor put down 4% on a conventional mortgage, then secured an 8% annual cash flow after expenses by targeting undervalued neighborhoods.

That translated to $800 in passive income every $10K of equity each year.

- Deal Screening Checklist: property condition, cap rate target, financing terms, exit timeline

- Due-Diligence Questions: tenant history, maintenance records, local market projections

- Cash-Flow Management Template: tracks rent, operating costs, loan amortization, repair reserves

Whether you use a simple spreadsheet or the PopaDex dashboard, monitoring yields and outstanding balances becomes second nature.

| Mortgage Type | Down Payment | Interest Rate | Leverage Ratio | Expected IRR |

|---|---|---|---|---|

| Fixed-Rate | 20% | 3.5% | 5x | 10–12% |

| Adjustable | 10% | 2.8% | 9x | 12–14% |

| Interest-Only | 5% | 2.5% | 20x | 14–16% |

Low rates between 2000 and 2020 tripled home prices across ten major economies, proving that property appreciation can power up your holdings. Learn more about these findings on McKinsey

Entrepreneurial Ventures That Scale

A founder turned a $10,000 seed round into a $2 million exit in four years by zeroing in on a specific SaaS niche.

Early revenue was reinvested into user acquisition via paid ads and strategic partnerships.

- Screening Criteria: market size, competitive landscape, revenue model clarity, customer acquisition cost

- Due-Diligence Questions: unit economics, burn-rate runway, founder equity splits

- Cash-Management Template: tracks monthly burn, runway extension, milestone-based spending

Most seasoned founders stress the need to adjust course before scaling too quickly.

“Fast exits hinge on clear value creation paths and aligned incentives.”

– Anonymous VC Advisor

Whether you choose an asset sale, a management buyout, or an IPO, each exit route carries unique tax ramifications that can boost your after-tax proceeds.

Planning Tax Efficient Exits

Swapping one property for another through a 1031 exchange lets you defer capital gains taxes while expanding your portfolio.

Founders often rely on Qualified Small Business Stock (QSBS) rules to exclude up to $10 million in gains, provided they hold shares for at least five years.

- Rollover Relief: redirect sale proceeds into replacement assets without an immediate tax bill

- Long-Term Gains: holding assets over 12 months unlocks lower tax brackets

- Early Advisory: bring in a tax specialist to match strategies with your planned exit timeline

Tracking And Reviews

Set up quarterly check-ins to compare projected vs. actual cash flow and growth.

PopaDex will alert you to over-borrowing or revenue dips so you can course-correct fast.

- Review ROI metrics each month to catch underperforming assets

- Adjust loan terms or reinvest dividends to maintain balance

Consistent monitoring ensures your borrowing strategy stays on track.

Checklists For Success

Combine real estate and startup milestones in one unified roadmap, complete with review dates and action items.

With PopaDex you’ll see rental income, loan balances, equity stakes, and projected exit values all in one place.

- Weekly: verify mortgage covenants to avoid surprises

- Monthly: assess burn rate to fine-tune expenses

- On Each Funding Round: track dilution to maintain ownership goals

Following proven frameworks means you won’t have to reinvent the wheel. Pair these tactics with disciplined reinvestment and you’ll witness step-by-step wealth acceleration.

Final Growth Steps

Before the quarter ends, revisit combined property and startup metrics to lock in improvements.

Use the PopaDex net worth tracker to merge home valuations, equity positions, and loan schedules into one unified view.

Adjust your roadmap as markets shift and only fund new ventures when your core yields stay above target.

Manage Risk And Track Wealth Progress

Fast wealth-building demands bold moves, but without a safety net, even a small setback can derail you. You can chase high returns, but they’ll count for little if you panic during a market swing. Here, I share tactics I rely on to cap losses and maintain momentum.

To guard against a sudden crash, I never let any single position dominate my portfolio. I rely on stop-loss orders to protect gains or limit setbacks. Periodic rebalancing then nudges everything back toward my chosen risk targets.

- Cap sector or security exposure at a predetermined maximum

- Configure stop-loss triggers around 10–15% below the highest price

- Reserve time each quarter for a comprehensive portfolio check

“Quarterly checks saved me from a 30% drawdown in 2022,” says one investor.

Risk Management Tactics

Reviewing performance every quarter shines a light on laggards before they balloon into a problem. I once noticed my tech holding slipping, so I cut it from 25% down to 15%. That tweak kept my overall volatility around 8% rather than letting it jump past 12%.

A written rulebook kills emotional trading. In my case, I set if-then alerts—either in my broker’s platform or via PopaDex—that tell me precisely when to take action. Clear thresholds remove doubt and speed decision-making.

- Define your personal drawdown limit

- Apply stop-loss orders on highly volatile assets

- Reset weights when allocation drifts more than 5%

Using Tracking Tools

I rely on visual tools to keep the big picture front and center. A good dashboard answers “Where am I now?” and “What if…?” in seconds. You can explore our Net Worth Dashboard to see assets, liabilities, and milestones at a glance.

To get started:

- Securely link your bank and brokerage accounts

- Assign asset categories and set your target allocation

- Estimate cash flows and key financial deadlines

- Turn on alerts for any allocation or drawdown thresholds you choose

Most dashboards track net worth trends, asset mix by class, and progress bars toward your objectives. I like embedding screenshots in my quarterly review—it makes the numbers pop.

“Seeing your net worth plotted monthly turns vague hopes into precise targets.”

| Feature | Purpose | Alert Threshold |

|---|---|---|

| Asset Allocation View | Compare actual vs. target weights | ±5% Drift |

| Cash Flow Forecast | Predict surplus or shortfall | <$1,000 Monthly |

| Drawdown Tracker | Monitor peak-to-trough declines | 15% max |

| Liquidity Buffer Check | Ensure emergency fund coverage | 3–6 months |

Stress tests are my secret weapon for uncovering lurking dangers. You might run a 20% market slump scenario to see if your cash buffer can handle margin calls and monthly bills. Running these simulations every three months shows if you’d survive a sudden drop.

Keep a liquidity reserve equal to roughly three to six months of expenses. I stash that in cash or ultra-short-term bonds so I’m never forced to sell long-term holdings at a loss. And as your budget or portfolio grows, top up this fund.

Stress testing is like a fire drill for your finances – it prepares you before disaster strikes.

Stress Test Scenarios

When I layer in different worst-case scenarios, I often see hidden weaknesses before they bite. In one run:

- Scenario A: 20% equity crash in a 60/40 portfolio

- Scenario B: 25% slump in real estate holdings

- Scenario C: A sudden credit freeze prompting margin calls

After running these, one retiree discovered a potential 15% drop in net worth if both markets tumbled together. They used that insight to expand their liquidity cushion from six to nine months of expenses.

Regular stress tests build confidence and expose correlations you might otherwise miss.

Maintaining Momentum

Staying in touch with your numbers keeps momentum alive. A quick monthly glance at your PopaDex net worth chart can spark small but powerful course corrections.

With clear drawdown limits, automated notifications, and reliable tracking in place, you’ll know instinctively when to stand firm or adapt your plan. That habit of disciplined monitoring separates serious wealth builders from the rest.

Keep tweaking your personal risk and tracking approach as markets and life circumstances evolve.

Frequently Asked Questions

Building wealth fast often triggers a dozen “what ifs” around risk, timelines, and starting points. In this FAQ, we cut through the noise with straight-talk answers grounded in real results.

You’ll get concise, data-driven guidance alongside snapshots of actual strategies people have used to grow net worth sustainably.

Fastest Sustainable Growth Methods

For many, combining income boosts with disciplined saving and shrewd investing unlocks the biggest gains.

Take Alex, a solo consultant, who negotiated a 15% raise, tucked away 30% of every paycheck, and added weekend gigs. In just two years, his net worth jumped by $50K.

- 10–20% pay bump: Document your accomplishments and ask for the increase.

- Weekend hustle: Launch a low-cost side project—coaching, digital tools, or consulting.

- Automated savings: Send 20% of each deposit into a separate account before bills hit.

By mixing two or more income streams, you spread your risk and accelerate compound growth.

Starting Capital Benchmarks

You don’t need six figures on day one. Small bets can snowball.

One reader invested $500 in a tutoring side-gig and turned it into $5K within twelve months.

Small amounts, when reinvested consistently, become powerful wealth engines.

- Side gigs: launch for $100–$500.

- Equity plays: start around $5K–$10K.

- Real estate or startups: budget $20K+ for meaningful entry.

Balancing Growth And Protection

Chasing higher returns without guardrails can erode your core capital. Begin by stashing a 3–6 month expense buffer in cash or ultra-short bonds.

- Maintain your emergency fund and review quarterly.

- Place stop-loss orders about 10–15% below recent peaks to cap potential losses.

- Adjust your buffer after pay raises, new side gigs, or major life changes.

These simple checks keep aggressive strategies from spinning out of control.

Timelines For Doubling Net Worth

If you consistently earn 12% annualized returns, history shows you can double your wealth in 5–8 years.

High-conviction equity bets or a breakout business can accelerate that to 3–5 years, but come with higher volatility.

“Grounding your timelines in real case studies keeps expectations realistic.”

Ready to see these strategies in action? Start tracking your progress effortlessly with PopaDex.